Yesterday I attended the Kickstart Europe conference in Amsterdam, a conference that only has a 3-year record, but has established itself as one of the main conferences for the European Data Center Market attracting around 1200 participants from a variety of different co-location companies, partners, investors, etc. My key take-away from the conference is that the industry is finally putting the right emphasis on sustainability as a decision criterion in site selection and how it is driving the emergence of new data center hubs in Europe. Here are some of my personal reflections on the conference from the Norwegian point of view.

A blog post by Svein Atle Hagaseth, CSO in Green Mountain

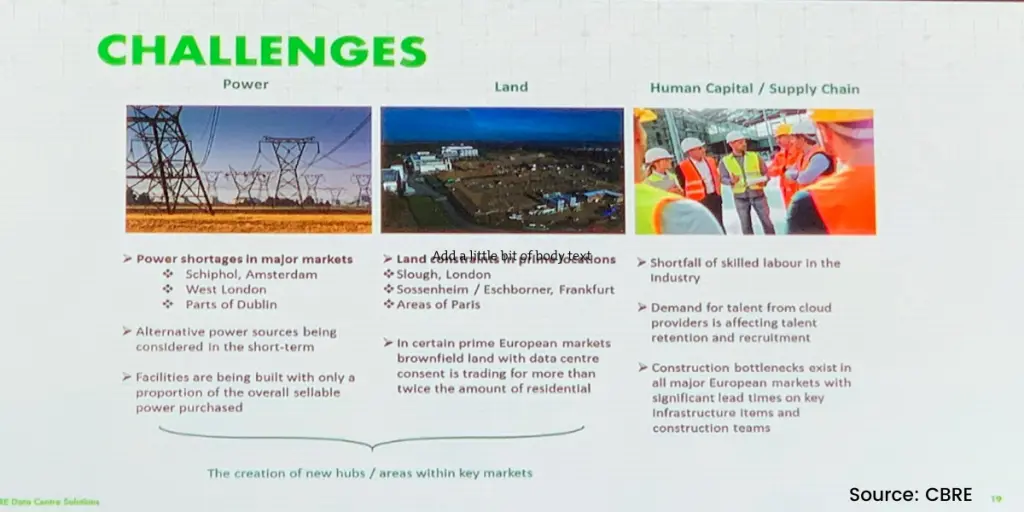

Challenges in the FLAP-D region

Mitul Patel from CBRE started the conference by sharing some valuable insights on the development in the FLAP-D* countries. He talked about why emerging hubs are popping up in new territories and countries because of the energy and land constraints in Amsterdam, Frankfurt, and London (see picture.)

This development is mainly driven by the ambition by the governments at these new hubs to provide green energy, a factor that not many countries have access to. In Norway, for instance, we are very fortunate to have an oversupply of green and available hydro energy, approximately 20 % overproduction, all green energy available to be used. In addition, Norway is a sparsely populated country with 12 persons per km², in comparison with for example the Netherlands with 507 persons per km² ** In other words, the availability of land and power for expansion is not an issue.

Skills and competencies

The increasing lack of a competent and specialized data centre workforce is also a topic often discussed. In Norway I think this challenge will be solved by our move away from Oil & Gas to other industries. This shift will push a substantial part of our skilled workforce into greener industries. Bringing with them strong skills and competencies in technology, automation, innovation etc. In Green Mountain we experience this already, being a “green company” we attract this talent.

Future growth

Mitul also mentioned in his predictions that he believes that we in 2020 will see the first 10 MW install outside of the FLAP-D region, something I truly agree on. I believe that the Nordics and Norway is willing and in a good position to be able to take a significant growth of the co-location market in Europe, mainly because there is a drive for sustainable solutions at a leading cost point. The growth outside the traditional FLAP-D market is also driven by the clients making more conscious decisions on where to store different types of data. It does not all have to be in FLAP-D, but where it makes more sense based on sustainability, cost and efficiency. I have said for a period of time that no-one ever got fired by choosing FLAP-D (based on the old saying, that no-one ever got fired by choosing big blue), but perhaps this is no longer the case?

The new players

In the leadership panel following Mitul’s presentation, there was an interesting discussion about how mature and well educated the marketplace is becoming, and that new players were willing to compromise on price and margins. In my opinion, I believe the new players are just better at finding the optimal solutions for the clients. They offer the acceptable level with full transparency. My experience as being one of these new players is that we have a sound business case for each and every opportunity we pursue. We look at the client individually and try to find the optimal solution rather than trying to push a given set of deliverables.

Difficult predictions?

Another concern that the panel raised was the increased difficulty in predicting where and how to build future capacity. In Green Mountain we experience the exact opposite. Our clients and prospects are more than willing to share their development plans and to propose where to go. The reason for this might be that we are ready to listen and offer the same type of openness in return.

To sum up, we all agree on the importance of sustainability but there seems to be a difference in the challenges the traditional and the new players in the market face. This may be an eye-opener to clients exploring the European data center market.

Svein Atle Hagaseth – CSO, Green Mountain

*FLAP-D = Frankfurt, London, Amsterdam, Paris, Dublin

*https://www.statista.com/statistics/264683/top-fifty-countries-with-the-highest-population-density/